FDIC Survey Shows Huge Potential for P2P Growth

Hi all, Julie here. Back from the apple orchard and ready to dive into fintech. In case you missed it, the latest FDIC survey came out about a week ago and showed us some obvious and not so obvious statistics on the current state of consumer banking in the US. Important to note off the bat: this survey is data from 2019...not 2020. It will be super interesting to check out this survey the next time it comes out (in 2 years...womp womp).

Anyways. The obvious stats first:

- If your mobile app sucks, your bank is doomed.

- Minorities are more likely to be unbanked.

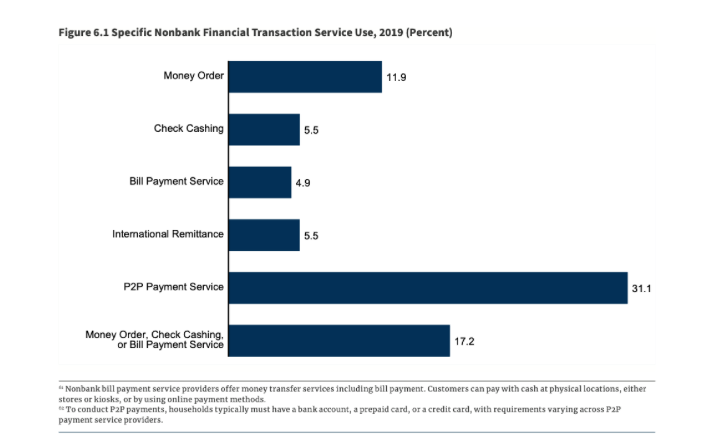

- Banked consumers used P2P more often than unbanked (you kind of have to have a bank to use a lot of them).

- People still don’t think banks are transparent on fees.

- Main reason for not having a bank is not having enough money to meet the minimum balance.

- People still don’t trust banks.

A not so obvious stat that I want to focus on this week: this was the first time the survey has included P2P. What?! Amanda Peyton, Co-Founder of Braid, pointed this out to me when we were going through the survey together. PayPal has been around since 1998, Venmo since 2009, Cash App since 2013. Wild.

The numbers here also surprised me a bit, with less than half of households using P2P services last year. Even without Covid I’d expect this number to be roughly double if not even higher in the next survey.

Now, this doesn’t mean that y’all should go out and build another fintech startup focused on P2P. It means y’all should probably go buy shares of PayPal or Square though (I do not give investment advice and this is just an analogy...meaning the current winners will just get bigger). And even though traditional banks have Zelle, I’m not sure they completely grasp the potential. Doing things like boosts or other promos just doesn’t feel like something Zelle would do, and that’s part of the draw for the P2P players that are winning.

“I don’t think the traditional banks understand how much P2P is growing and how much it still has to grow. Everyone has some use for a P2P product. I think there is going to be a huge spike in usage here.” -Amanda Peyton

Side bar: Facebook, if it had done a better job at a number of things, could have absolutely crushed it here. A massive customer base that has loads of connections where it can and should be easy to send money. But somehow, PayPal, Venmo and Cash App came out on top. There should honestly be a case study on this in a fintech course for any colleges offering that sort of thing (or something we should do? Email me if you think that’d be interesting/have thoughts/can help). You know how nice it would be to send money through Instagram or WhatsApp if I actually trusted them? Damn.

Anyways, another point Amanda and I talked about was how much more comfortable people are with having a number of financial accounts now. Gone is the era where 1-2 accounts was the standard. This is good news for the banks that are popping up, and they probably have a lot to do with it. People want to test out the accounts, grab any offers they might have like getting paid early or debit card boosts. But it also makes grabbing loyal customers a bit trickier. Right now, we probably have a lot of folks that are only using the debit cards these banks offer a few times a year in some cases. If that’s the case, that customer is going to take a long time to pay off the cost to acquire them in the transaction fee revenue model. On the other hand, it probably cost a bit less to acquire them in the first place if they’re so willing to have several accounts.

“If you look at certain age groups, seeing how many checking, brokerage, or financial accounts that age group has would be very interesting. It used to be that you’d have 1 or 2 accounts and now younger age groups could have 5, 10 or even 20.” -Amanda Peyton

This makes me wonder what people will really think of “banking” as in the future. We already associate these P2P products as a sort of bank account even though they’re not. Could banking also become almost invisible like payments have in many cases? Where the banking just sort of happens behind the scenes and we just get app updates or tik tok blurbs on what happened in our financial lives that day? Where else can these P2P products take away from traditional checking accounts?