Affirm's S-1 Shows Heavy Dependence on Peloton, But Does It Matter?

Hi all, Julie here. Remember when shares of Afterpay plunged earlier this year as investors grew concerned about the potential of rising defaults due to Covid? Well…fast forward to today and shares of the Buy Now Pay Later provider are near an all time high and a competitor just filed to go public. Another 2020 surprise…typical.

So, in the week before Thanksgiving, I got something that I am thankful for: a better look at Affirm’s financials. While there is a lot to take in over the course of a few hundred pages, something that quickly stood out to me was the large percentage of sales that Peloton accounts for. It’s not that it’s shocking, it’s just that we finally got an inside look at just how much of Affirm’s business is from financing fancy bikes and treadmills.

Side note: I’m doing a collab with The Generalist’s “S-1 Club”, so you should subscribe here to avoid missing it :)

Now, there are a slew of things you can derive from this: * Affirm has fewer repeat customers than the likes of Afterpay since people don’t buy Pelotons multiple times a year. * Losing Peloton as a customer would really hurt (they just renewed their contract though, so this is safe for the time being). * Loans are on Peloton’s books for longer than they are at the other providers in the space. * Afterpay, for instance, offers four payments over the course of eight weeks, while the average duration for assets currently retained on Affirm’s balance sheet is six months.

And speaking of the loan book, a friend who’s much smarter than me made an interesting point. Yes, it’s cool to have a better look at Peloton’s percent of sales, but what we’d really love to know is what Affirms delinquency rate would look like if we took out Peloton.

As it stands, the overall rate is low. From the S-1:

“Our continuously-learning risk model benefits from increasing scale. As data from new transactions are incorporated into our risk algorithms, we are able to more effectively assess a given credit profile. Our model is robust enough to allow us to assess credit risk at a pre-defined risk level with a high degree of confidence, resulting in a weighted-average quarterly delinquency rate of approximately 1.1% for the thirty-six months ended September 30, 2020.”

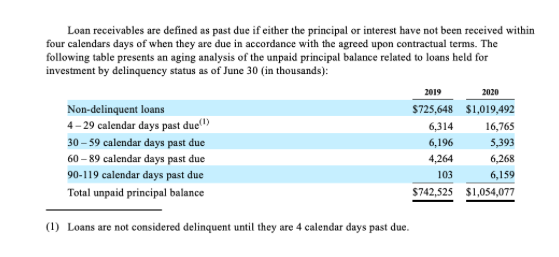

Here’s a look at just how far into delinquency the loans are as well. As you can see, there was a decent jump in the value of loans that were a month or less past due. However, loans 1-2 months late were actually down and loans 2-3 months late were pretty stable. Then again, there was a large jump in loans that were severely past due.

But what if you took out the folks that are buying an expensive bike or treadmill? Sure, I guess people could stop paying for exercise equipment, but it feels like if you’re the type of person that’s going to pay upwards of $1,800 for it, you’re probably going to pay it off. Peloton’s CFO in their May earnings call said:

“We had very consistent financing penetration over the last couple of months and as you can imagine I think we’ve talked about this before. We had to date extremely low default rates and a fairly healthy credit profile of a lot of those that participate in our financing programs.”

So I’d expect that the Peloton loans take the overall delinquency rate down, it’s just a question of how much. Let me say that I don’t think the portfolio would look terrible, and that’s largely because of the short loan duration. You see, not every purchase on Affirm is for a $2,000 bike, just a good chunk of them. More from the S-1:

“Because of the relatively short duration of our pay-over-time products, of the monthly loan vintages originated before the pandemic began in March 2020, only 19% remained on our balance sheet by the end of September 2020. As of September 30, 2020, our delinquency rates, as a percentage of our loan portfolio, and excluding the impact of our payment deferral program, were approximately 66% lower as compared to September 30, 2019. In addition, as of September 30, 2020, our gross charge-offs, as a percentage of our loan portfolio, and excluding the impact of our payment deferral program, were approximately 48% lower as compared to September 30, 2019.”

In general, the trend looks good, but companies are fully allowed to cherry pick data a bit for the S-1, which is why I’m interested in getting a more granular look at the loan book to make sure it is indeed as good as what they make it out to be.